Will Social Security Be There for You?

Examining the Fiscal Challenges and Legislative Solutions for Long-Term Solvency

One of the most pressing concerns for many Americans today is whether Social Security will be available when they retire. Given the numerous reports and discussions surrounding the fiscal health of the Social Security Trust Fund, it's a valid question that deserves a detailed exploration.

Over time, Social Security has become an increasingly critical component of retirement income for many Americans. Initially intended to supplement personal savings and employer-sponsored pension plans, Social Security now constitutes a significant portion of income for the majority of retirees.

Several factors have contributed to this shift, including the decline of defined benefit pension plans, stagnant wages that limit personal savings, and the economic instability that has eroded other forms of retirement income.

As a result, Social Security has become a lifeline for millions of seniors, providing essential financial support in their retirement years. This increased reliance underscores the urgency of ensuring the program's solvency and sustainability for future generations.

The Current Fiscal Situation of the Social Security Trust Fund

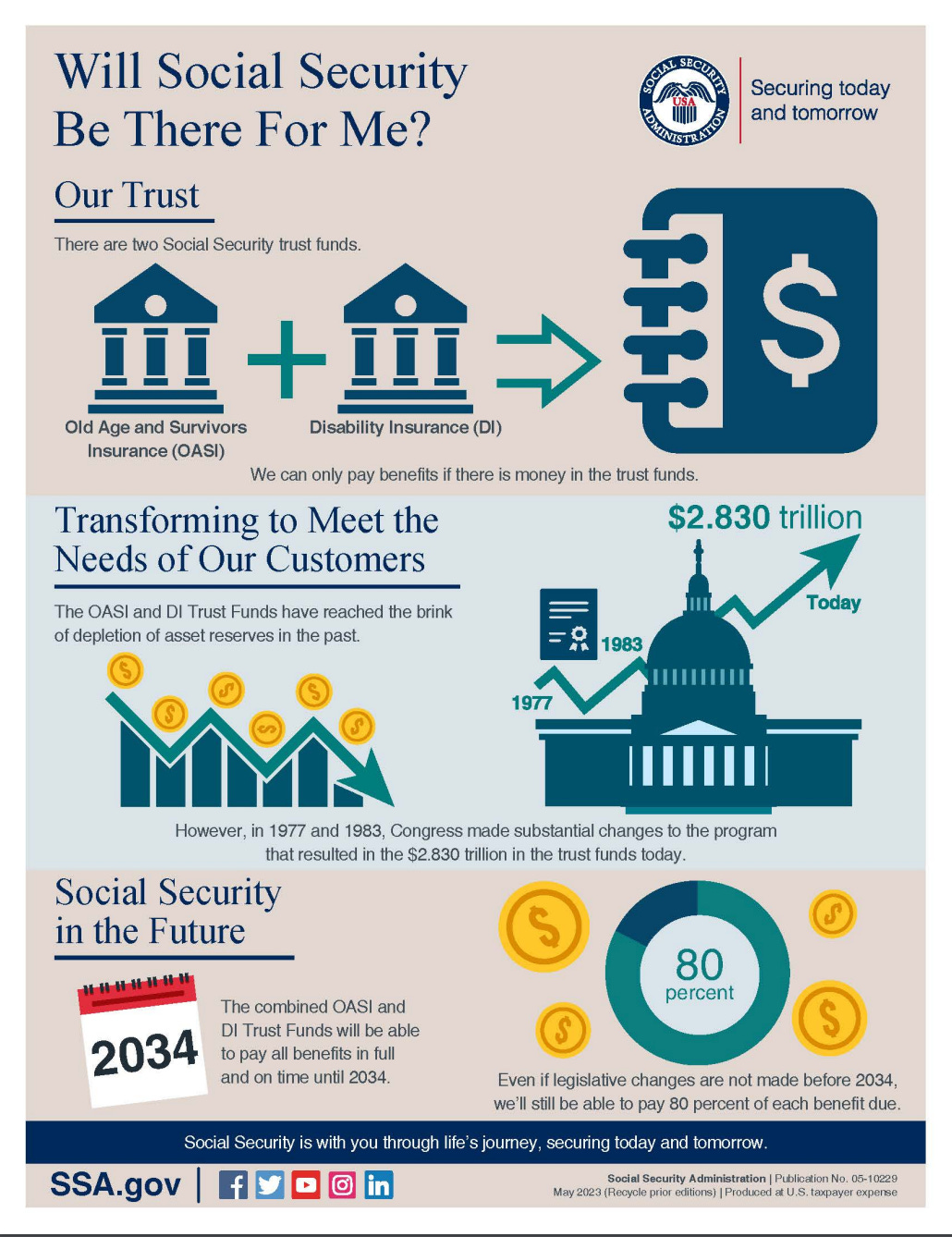

The Social Security Trust Fund, established to ensure that retirees receive their benefits, faces significant financial challenges. As it stands, the trust fund comprises two main components: the Old-Age and Survivors Insurance (OASI) Trust Fund and the Disability Insurance (DI) Trust Fund. These funds are primarily financed through payroll taxes collected from workers and employers.

For every year from 1983-2020, Social Security has collected more revenue than its total costs; resulting in a nearly $3 trillion surplus. However, since 2021 total costs have exceeded revenue. In 2023, workers contributed $1.233 trillion to the fund, and payments to beneficiaries amounted to $1.379 trillion. The trust funds’ reserves supplement the program’s income — from payroll taxes, income taxes on benefits paid to higher-income beneficiaries, and interest earned on the trust funds’ bonds — to enable Social Security to continue paying full benefits until 2034 if no legislative action is taken.

Several factors have strained the trust fund's solvency:

Demographic Changes: The aging baby boomer generation is retiring in large numbers, resulting in more beneficiaries than ever before. Baby boomers, born between 1946 and 1964, represent a substantial portion of the U.S. population.

As they reach retirement age, the number of people drawing benefits from Social Security has surged. Concurrently, birth rates in the U.S. have been declining for decades. This decline means there are fewer workers entering the workforce to replace those retiring, leading to a reduced number of contributors to the Social Security system. This demographic shift creates a significant imbalance, as more funds are being paid out in benefits than are being collected through payroll taxes.

Increased Life Expectancy: Advances in healthcare and living standards have resulted in people living longer, which, while a positive development, also means they collect benefits for a more extended period. When Social Security was established in 1935, the average life expectancy was significantly lower than it is today. The system was designed with the assumption that beneficiaries would collect payments for a relatively short period. However, modern retirees can expect to live many years, even decades, beyond the traditional retirement age, placing additional strain on the trust fund. This increased longevity means that the funds must cover more extended periods of benefit payments, further depleting the reserves.

Wage Stagnation: Wage stagnation means that the taxable earnings of workers have not increased significantly over time. Since Social Security payroll taxes are capped at a certain income level (currently $160,200), the impact is even more pronounced. High-income earners, whose wages often grow faster and who benefit more from economic growth, contribute the same maximum amount regardless of how much their income increases above the cap. When wages stagnate, the total payroll tax revenue grows more slowly. Given that Social Security benefits are funded primarily through these taxes, any slowdown in revenue growth translates into financial stress for the program.

Ensuring Solvency: Advocating for the Social Security Expansion Act

To address these challenges and ensure that Social Security remains solvent for future generations, it is crucial to advocate for legislative solutions like the Social Security Expansion Act (S.393). This bill, introduced by Senator Bernie Sanders—for himself and nine additional senators, aims to strengthen and expand Social Security by implementing several key measures:

Raising the Payroll Tax Cap: Currently, payroll taxes are only collected on the first $160,200 of earnings. S.393 proposes to apply the payroll tax to incomes over $250,000, ensuring that high earners contribute a fairer share to the system.

Cost-of-Living Adjustments (COLA): The bill would adopt a more accurate measure of inflation for seniors, the Consumer Price Index for the Elderly (CPI-E), ensuring that benefits keep pace with rising costs.

Increasing Benefits: S.393 proposes increasing benefits for all recipients by $200 per month, addressing the growing economic insecurity faced by many retirees.

Expanding Benefits for Low-Income Workers: The bill includes provisions to boost benefits for low-income workers, ensuring that those who have spent their careers in low-wage jobs are not left behind.

Why This Matters

Passing a bill like the Social Security Expansion Act is essential for several reasons:

Economic Security: Social Security provides a vital safety net for millions of Americans. This program was established to protect retirees from poverty by ensuring they have a source of income after they stop working. Currently, nearly 65 million people receive Social Security benefits, including retirees, disabled workers, and their families. For many, Social Security represents the primary source of income during retirement, offering stability and predictability that other retirement savings options may not provide.

Reliance on Social Security: About half of elderly beneficiaries rely on Social Security for more than 50% of their income, and roughly one in four depend on it for at least 90% of their income.

Poverty Prevention: Without Social Security benefits, an estimated 22 million Americans would fall below the poverty line, including over 15 million seniors.

Economic Stability: By providing a stable source of income, Social Security helps maintain consumer spending among retirees, which supports the broader economy.

Addressing Inequality: The proposed changes help address economic inequality by ensuring that high earners contribute more and by boosting benefits for low-income workers. The Social Security Expansion Act proposes raising the payroll tax cap so that those with higher incomes contribute a fairer share. This adjustment recognizes that income disparity has grown significantly over the past few decades, with most economic gains benefiting the wealthiest individuals.

Fairer Contributions: Currently, individuals earning above the payroll tax cap contribute a smaller percentage of their total income to Social Security compared to lower and middle-income workers. Raising the cap ensures a more equitable distribution of the tax burden.

Benefit Increases: The proposed $200 per month increase in benefits would significantly impact low-income retirees, providing them with greater financial security and reducing economic disparities in retirement.

Economic Mobility: Strengthening Social Security can help mitigate the long-term effects of wage stagnation and economic inequality, promoting greater economic mobility and stability for future generations.

Intergenerational Fairness: Ensuring the solvency of Social Security is not just about current retirees but also about providing future generations with the same level of support. The financial challenges facing Social Security threaten to reduce benefits for future retirees unless addressed promptly. By implementing reforms like those in the Social Security Expansion Act, we can ensure that the program remains robust and reliable for decades to come.

Future Security: Younger generations, who are currently contributing to Social Security through payroll taxes, need assurance that the program will be there for them when they retire. Addressing solvency issues now prevents a future crisis.

Confidence in the System: Strengthening Social Security boosts confidence in the program, encouraging younger workers to continue supporting it through their contributions.

Legacy of Support: Social Security was designed to be a social insurance program that spans generations. Ensuring its longevity preserves the intergenerational contract that has been a cornerstone of American social policy since the New Deal era.

“We can never insure one hundred percent of the population against one hundred percent of the hazards and vicissitudes of life, but we have tried to frame a law which will give some measure of protection to the average citizen and to his family against the loss of a job and against poverty-ridden old age.”

-Franklin D. Roosevelt

Social Security is a cornerstone of economic security for millions of Americans, providing essential support to retirees, disabled workers, and their families. However, the program faces significant financial challenges that must be addressed to ensure its continued viability. By advocating for legislative measures like the Social Security Expansion Act, we can address these challenges, promote fairness, and secure the program's future for generations to come.

To ensure Social Security remains a robust and reliable source of income for working people as it was intended, it is crucial that we take action.

Here are some steps you can take:

Contact Your Legislators: Reach out to your senators and representatives to express your support for the Social Security Expansion Act. Let them know that preserving and strengthening Social Security is a priority for you and your community.

Engage with Candidates: When considering candidates for federal office, ask about their positions on Social Security. Support those who are committed to protecting and expanding the program.

Stay Informed: Keep up-to-date with developments in Social Security policy and share this information with friends and family. Educating others about the importance of this issue can help build broader support.

Vote: Participate in elections and support candidates who prioritize the strengthening of Social Security. Your vote can make a difference in ensuring that the program continues to provide financial security for future generations.

By taking these actions, we can help secure the future of Social Security and ensure that it continues to fulfill its promise of providing economic stability and reducing inequality.